Dairy Reports

Dairy Council Report September 2020

July Milk Price Update

- Glanbia: Base price of 29.68c/L for creamery milk at 3.6% fat and 3.3% protein. Farmer members will receive an additional 0.42c/L as their share of GI Profit. Totalling 30.1c/L.

- Lakeland Dairies: Base price of 31c/L, up 1c from June price.

- Kerry: Base milk price of 30.5c/L. No change from price announced last month.

- Barryroe Co-op: Variable milk price for July is unchanged at 32.76c/L at 6% fat and 3.3% protein, including SCC bonus, VAT and 1c from Carbery stability fund.

- Arrabawn: Increased the price to 31c/L including VAT, an increase of 0.5c/L.

- Dairygold: Increase of 0.5c/L for its July quoted milk price to 30.69c/L, based on standard constituents of 3.3% protein and 3.6% butterfat, inclusive of bonuses and VAT.

- Aurivo: Paying a milk price of 31 cent including vat for July milk.

- Carbery: Carbery is maintaining its milk price for July. If this decision is replicated across the four West Cork co-ops; Bandon, Barryroe, Drinagh and Lisavaird, this will result in an average price for July of 31.9cpl, inclusive of VAT. 1cpl in support continues to be paid from the stability fund. The price is exclusive of SCC or any other adjustments which may be made by the co-ops.

Market Report

- The most recent dairy market report by Catherine Lascurettes is attached for greater detail.

- The GDT Index has experienced three consecutive declines, with a reduction of 1.7% following the latest event on August 18th. This comes after a 5.1% drop on August 4th. Drops in the index were across the board with the exception of BMP (wasn’t offered) and SMP, which increased by 1.1% to an average price of US$2,608/MT. Serious trading decisions regarding the really heavy trading period – the last quarter of 2020 and first of 2021 – which gathers most of the demand promoting events and religious festivals (Thanks Giving, Christmas, Passover, New Year, Chinese New Year, Easter, Ramadan…) will start from autumn, after the summer holiday period. So, we should not read too much in this month’s GDT results.

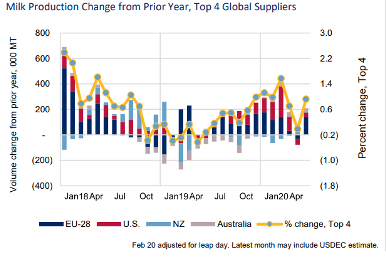

- Global milk supplies had been subdued up to May but are now picking up. The EU Commission has predicted an overall increase 0.7% for 2020, which suggests tighter supplies for the remaining months. Europe’s market fundamentals have been relatively well balanced with good milk supplies and strong exports. EU-28 milk collections for June the were up 1.2% putting collections for the first half of 2020 1.6% ahead of last year. Strong year-on-year gains for Poland [+4.6%] and Ireland [+2.9%] helped drive the June volume higher. Germany, the Netherlands and the UK saw less significant year-on-year increases for the month. Domestically, the milk intake for the month of July was 4.4% higher than the same month for 2019, according to the latest CSO statistics. Taking the first seven months of the year as a whole, approximately 5.4 billion litres were taken in for that period, compared to around 5.2 billion litres in the same period of 2019, for an upwards change of 3.8%. Production of butter in July 2020 stood at 30,360t, an increase of 7.5% on the July 2019 figure of 28,200t. Meanwhile, skimmed milk powder production stood at 19,650t in July of this year, an increase of 2.9% on the 19,100t in July of last year.

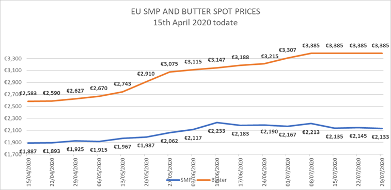

- After six consecutive weeks of price stability, the European butter quotation finally made a move, albeit small, to the upside last week (+0.2%), according to multi-national financial services firm StoneX. The European butter quotation has now gone 19 weeks since it last saw a move lower, posting 13 weeks of gains in that period sitting at €808 [+31%] above where it was in mid-April, but €248 [-7%] below where it was at the end of January. EEX butter futures meanwhile have pushed higher in recent weeks with the September 2020 to April 2021 contracts up 2.6% on average over the last three weeks. The stable to firm price action in Europe came about despite the ongoing weakness for fats in the GDT auctionin New Zealand which saw butter (-2.0%) and anhydrous milk fat (-2.9%) both move lower.

- On the milk powder front, the European SMP index was higher this week, gaining 1.3%, reversing almost half of the declines posted in the previous four weeks. EEX SMP futures have also posted strong gains over the last few weeks with the front six months up 5% over the last three weeks. NZ SMP also saw some support [+1.1%] in the most recent GDT auction, although price weakness for WMP [-2.2%] which accounts for the largest proportion of product offered on the platform contributed to the overall index moving down by 1.7%.

New PPI

- The first important thing farmers should understand is that the prices paid by Ornua to co-op for dairy products will not be changed in any way by the changes to the PPI. To be absolutely clear, Ornua will not be paying any less for the products co-ops sell through them, and the new PPI should, objectively, have no influence on co-ops’ ability to pay a competitive milk price.

- The second thing is that the PPI will now reflect commodity returns only.

- The third important information is that the value of premium, non-commodity products traded for the month, together with the value for the month of the trading bonuses co-ops used to receive only annually in the past, will now be shown below the line.

Combined, these two values will be called the Ornua Value Payment (OVP). While the trading bonuses are achieved partially on the trade by Ornua of non-Irish products, they are an actual payment to all co-ops that trade through Ornua. The OVP will be paid monthly, generating a value which also contributes to the co-ops’ milk price payment capacity. - Ornua have decided to express the OVP as a single global monthly € amount, and a percentage of gross purchases in the month.

- To help farmers better gauge the real value to co-ops of the OVP in terms that they can readily appreciate, IFA will endeavour every month to estimate that value in terms of the cents per litre it adds to the milk price equivalent of the PPI calculated by Ornua.

Activity since last Council

- IFA met with the DAFM to discuss the issue of live exports and ferries willingness to transport animals. Alternative option of flying calves out of Shannon was discussed.

- IFA met with Bord Bia in relation to the return of physical auditing.

- IFA met with DAFM in relation to N derogation review.

- IFA met with Teagasc to discuss a resolution from Cork Central on the Teagasc Profit Monitor.

Upcoming issues

- Within the coming weeks, co-ops will be determining their August milk prices. IFA will monitor developments and communicate those, which we hope will continue on the current positive trend, to officers and members. The total reduction in income across primary agriculture in Ireland in 2020 is projected to range from 0.7billion to 1.6billion. In absolute terms, the reduction in average farm incomes is projected to be largest on dairy farms.

- Collaborating with National Environment Committee in relation to the N derogation review. Change in calculation of Nitrates per cow from 85 to 89 should be left until January 2022 to give farmers the chance to plan accordingly.

- IFA will continue to state PPI in c/L.

| Chairman | Tom Phelan |

| Policy Officer | Anna Daly |