Farm Business Council Report November 2025

IFA Submission on Finance Bill 2025

VALUE-ADDED TAX

Section 65

The Finance Bill, which is published in the days following the Budget announcement gives legislative standing to many details of the Budget, usually to take effect from a later date, often the following 1st January. Broiler farmers were subject to an order by the Minister for Finance in July 2025 S.I. No. 327 of 2025 – Value-Added Tax (Restriction of Flat-Rate Addition). This order removed the broiler sector from the flat rate addition (FRA) scheme from 1st September 2025. Changes to Section 65 of Value Added Tax legislation in the Finance Bill 2025 give the effect of forcing all commercial (and free range) broiler farmers to register for VAT from 1st January 2026.

This change represents a fundamental departure from the purpose and spirit of the flat-rate scheme, creating unnecessary administrative and financial burdens for family farms. It will do likewise for accountants, and Revenue Commissioners. It affects all c.445 commercial and free-range broiler farmers.

IFA is registering a strong objection to the inclusion of points (vi) and (vii) under Section 65 (“Persons not accountable persons unless they so elect”) of the Finance Bill 2025.

Legislative Background

Section 65 of the Finance Bill 2025 proposes to amend Section 6(1)(a) of the Value-Added Tax Consolidation Act 2010 by adding two new clauses:

(vi) agricultural services of the kind specified in an order made under section 86A, the total annual turnover for which has not exceeded the services threshold, or

(vii) agricultural produce of the kind specified in an order made under section 86A, the total annual turnover for which has not exceeded the goods threshold;”

These clauses give legislative effect to S.I. No. 327 of 2025, which from 1 September 2025 removes from the flat-rate addition “the supply of any agricultural service of stock minding, rearing and fattening in the course of the production of broiler chickens.” It did not remove them from operating as flat rate farmers which is critically important to their operation as mixed family farms.

The combined effect of these measures is that broiler farmers will no longer be entitled to apply the flat-rate addition and will be forced to register for VAT if they continue to supply those services, or goods, due to the threshold limitations.

This marks a significant policy shift that disproportionately impacts one specific group of farmers -broiler producers. This is an unwelcome precedence that IFA object to.

Practical and Economic Implications

The impact of this legislative change will be extensive, particularly for family-run mixed farms operating across multiple farming businesses. IFA highlights the following key concerns:

- Separation of Farm Enterprises

- Increased Cashflow Pressures

- Financial and Professional Costs

- Administrative Burden on Revenue

IFA Position

- Poultry farmers should retain the option to elect to register for VAT where they choose.

- VAT registration should not be imposed as a compulsory measure on a specific class of farmers.

- The flat-rate scheme must remain a practical, workable mechanism that protects family-run farms from unnecessary bureaucracy.

The IFA has engaged constructively and consistently with both the Department of Finance and the Revenue Commissioners to find solutions that are proportionate, transparent, and achievable for farmers on the ground.

Residential Zoned Land Tax

Budget 2026 gives another opportunity for landowners subject to RZLT in 2026 to request a change from their Local Authority in the zoning of their land and avail of an exemption from RZLT liability.

“There will be an exemption from the 2026 RZLT liability if a landowner applies for a rezoning to reflect the “genuine economic activity currently being carried out on the land”.

This remains a temporary solution from a tax that is unfair to genuine farmers of land that falls within the scope of RZLT. Responsibility to gain the exemption, and the cost associated with gaining the exemption falls back on the landowner.

IFA has campaigned to have a permanent solution that will remove actively farmed land from the scope of Residential Zoned Land Tax. This remains the policy of IFA.

IFA position remains that landowners with declared agricultural activity must be removed from the scope of Residential Zoned Land Tax.

Engagement with Banking Sector and Livestock Marts

IFA hosted representatives of the Mart Forum with ICOS and independent operated marts, The Property Services Regulatory Authority (PSRA), in the Farm Centre on Thursday 31st October. This was to emphasise the importance of maintaining our livestock mart trade, as credit transfer mechanisms evolve, while maintaining the usage of cheques by farmers.

Farm Finance

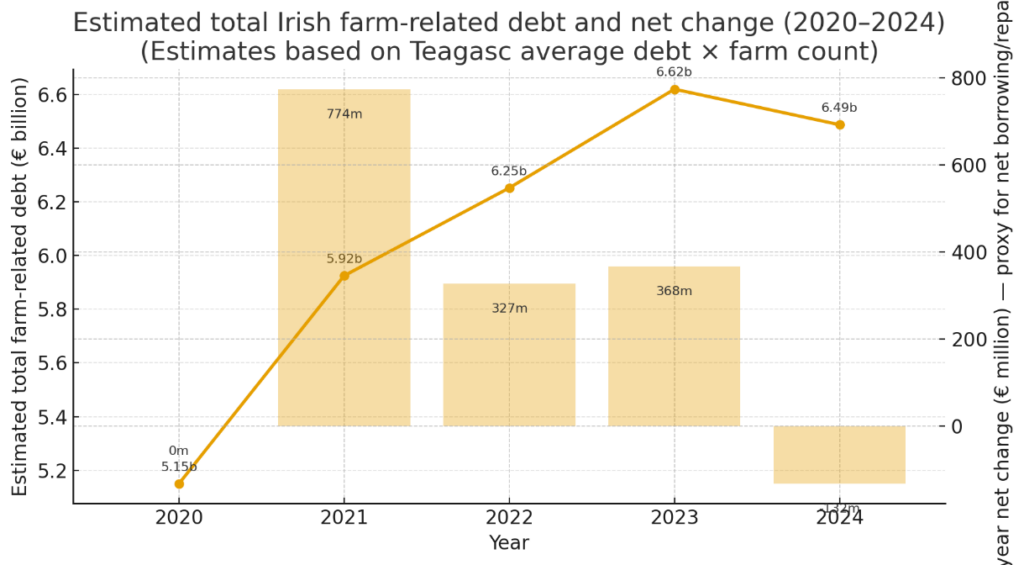

Credit to the farming sector is regularly raised with the mainstream banks by IFA, as farmers must continuously invest in infrastructure, stock, machinery and working capital on farms. The period 2024 – 2025 has been positive in terms of cashflow on farms with overall farm debt in the sector reducing.

Total farm debt reduced in 2024, as new investment drawdown slowed relative to paydown and reports from the banking sector report the first 6 months of 2025 continued this trend. As farm debt is paid off, the rate of new lending, which is increasing is not keeping up with this paydown rate over the past 2 years. This can be largely attributed to uncertainty over the future of the Nitrates Derogation.

Lending to poultry and pig sectors increased over the past 24 months with both new builds in poultry and replacement or refurbishment of existing sites in the pig sector accounting for most of the new lending.

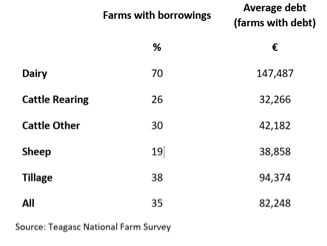

Looking at farming sectors, dairy remains the biggest driver of farm finance applications.

The drystock sector has seen a reduction in overall debt following positive income returns in 2024-25 and continued reduction in new lending. The relatively low percentage of farms with farm debt can be attributed to the high percentage of part-time farmers in the cattle and drystock sectors.

Sheep farming has contracted significantly in number in the past 2 years, and investment has followed this trend.

Tams grants are seen a major driver of loan applications and future agri investment on all farms.

Credit Review

IFA meeting Credit Review.

Established in 2010 By the Minister for Finance to ensure the continued flow of credit to all viable Irish businesses including farmers. Farmers who have been turned down for credit applications can apply for their application to be reviewed and resubmitted with a recommendation from the Credit Review financial team. Credit experts within the Credit Review assess the viability of cases and assist in re-applications and make recommendations where around 80% of applications to credit review get favorable decisions.