Pig Council Report February 2026

Market Report

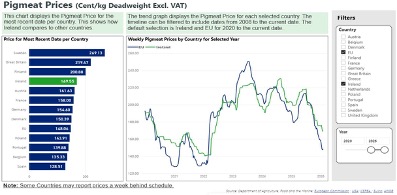

When the last council report was submitted in November prices (including vat) were as follows: Rosderra €1.86 – 1.90c/kg

Kepak €1.86 –1.90c/kg Dawn P&B €1.86- 1.90c/kg Staunton’s €1.86 – 1.90c/kg Sows €1.15/kg

Today, as we enter the 2nd week in February 2026, the average pig price reported by Irish pig farmers is €1.76/kg including VAT.

Rosderra €1.74 – 1.84c/kg (Grading system) Kepak €1.74 –1.78c/kg

Dawn P&B €1.74- 1.78c/kg Staunton’s €1.74 – 1.78c/kg Sows €0.98/kg

When the previous Council report was submitted in November, pig prices had already come under significant downward pressure following the sharp market correction experienced from early July onwards. At that time, prices paid by processors (including VAT) were broadly aligned across plants, with quotes in or around €1.84/kg-€1.86/kg observed. It should be noted that Rosderra introduced its grading-based pricing system in early December, with payments adjusted according to carcass weight and lean meat percentage under its Pig Quality Payment System (PQPS). While some producers report improved returns under the new system, others indicate reduced payments depending on pig specification, resulting in mixed outcomes at farm level.

Since then, further price erosion has occurred. As of the second week of February 2026, the average pig price reported by Irish pig farmers has fallen to approximately €1.76/kg including VAT, representing a reduction of around 10–14c/kg compared with November levels. This decline has significantly tightened producer margins at a time when costs remain elevated. The reduction in sow prices is particularly notable, with returns down by approximately 17c/kg since November.

While Ireland continues to maintain a premium relative to the EU average pig price, the narrowing of this differential highlights the extent to which domestic prices are being influenced by broader European market conditions, weak export demand, and ongoing uncertainty related to animal disease and trade disruption. The current price levels leave many producers operating close to, or below, breakeven, raising concerns regarding confidence, reinvestment, and longer-term production capacity within the sector.

Final slaughter data for 2025 confirms that Irish pig throughput increased again year on year, continuing the upward trend observed throughout the year. Total pigs slaughtered in the Republic of Ireland in 2025 are estimated at approximately 3.26 million head, representing an increase of just over 3% compared to 2024.

Sow slaughtering’s for the year amounted to approximately 92,450 head, also showing an increase on the previous year. Elevated sow throughput, particularly in the second half of the year, reflects ongoing structural adjustment within the sector as producers respond to sustained margin pressure and market uncertainty.

Throughput remained relatively steady on a weekly basis during the final quarter of the year, with no significant seasonal uplift evident. This consistent supply, combined with weaker export demand and downward pressure on EU prices, has contributed to the difficult price environment experienced since mid-2025.

Live exports to Northern Ireland also increased during 2025, rising by approximately 12% year on year, contributing to higher overall pig flows on an all-island basis. However, market feedback indicates that demand for live exports eased towards the end of the year and into early 2026.

For Grade E pig carcasses, the EU weighted-average price for the week ending 1st of February 2026 stood at roughly €1.48/kg (this was €1.59/kg in Nov) representing a continuing downward trend across the bloc. In comparison, Irish producers achieved an average of approximately

€1.80/kg, for the same week. The Chinese tariffs which apply to EU pigmeat exports into China are not helping matters although those levels have reduced significantly since before Christmas.

Latest trade data for the period January to November 2025 indicate a mixed performance for Irish pigmeat exports, with overall volumes and values easing slightly year on year, alongside notable variation across product categories.

Total pigmeat export value for the period amounted to approximately €425.2 million, representing a decline of €29.7 million (–6.5%)compared with the same period in 2024. Export volumes totalled approximately 181,641 tonnes, down 2.8% year on year. The reduction in overall export returns reflects a combination of lower market prices, weaker demand in certain destinations, and challenging trading conditions across the EU and international markets.

Latest Kantar data to December 2025 show that domestic demand for pigmeat remained relatively resilient. Average retail pork prices declined through much of 2025 before increasing again towards the end of the year, with the average multiple pork price rising to approximately

€7.87/kg in December.

Retail volumes remained stable, with consistent demand for core products such as pork chops and mince, while bacon and ham volumes were broadly steady. Pigmeat maintained or increased its share of both spend and volume across the major retail multiples, continuing to perform well relative to competing proteins. Overall, while retail demand and pricing strengthened modestly towards year end, this did not translate back to farm-gate prices, which continued to weaken into early 2026.

Activity since last National Council

- Engagement continues with the Nitrates Division on the proposed four-day rule, with the Committee stressing the logistical impossibility of the measure for integrated pig units and live slurry movements. We have sought to use the previous years data to inform import capacity. This has not been accepted but we continue to engage with the Nitrates Division on same.

- Ongoing discussions are taking place with DAFM, Animal Health Ireland, the EPA, Meat Industry Ireland, processors (on pricing mechanisms), and Bord Bia to address immediate market challenges and promote long-term sector viability.

- Continued close cooperation with the Food Regulator, Niamh Lenahan, to strengthen transparency and fairness in the pigmeat supply chain.

- DNA testing and traceability work continues in the foodservice sector to ensure Irish-produced pigmeat is used wherever possible. The Committee has renewed focus on retail compliance and visibility of Quality Assured Irish product which is an area of particular importance.

- Retail engagement remains active on pricing, sustainability, and evolving production standards to ensure the viability of domestic pig farming.

- Ongoing technical discussions with the EPA and the Commission regarding IED implementation.

EU/COPA Developments

- Continued collaboration with Copa-Cogeca and the European Commission on simplifying the implementation of the Industrial Emissions Directive (IED) to reduce administrative burdens on pig farmers.

- Ongoing engagement with Copa-Cogeca on the revision of the Animal Welfare in Transport Regulation, and animal welfare of farmed animals contributing to position papers to ensure practicality for Irish producers.

- Monitoring the “End of Cages” initiative, with Copa-Cogeca’s impact assessment warning that an immediate implementation could remove up to 37 % of EU pork output and 3 % of egg production, underlining the need for phased, realistic transition periods.

- Engagement with Copa-Cogeca and DAFM on the EU Deforestation Regulation (EUDR), now postponed to December 2026. The IFA is emphasizing the importance of safeguarding feed supply chains, particularly for imported soy used in pig rations.

- Participation continues in the EU Horizon “WelFarmers” project, where IFA pig representatives are contributing to thematic groups on farm welfare practices and knowledge exchange across regions.

Upcoming Issues

- We are working on arranging a further follow-up meeting with the Nitrates Division (DAFM).

We met on the 4th of December, and further discussions are needed to secure practical amendments to the export/import of nutrients.

- Market pressures persist: the average Irish pig price is currently around €1.76/kg. The Committee will continue engaging with processors to push for fairer price returns and transparency in contract structures.

- Renewed focus on reducing imported pigmeat use in the foodservice sector and improving presentation and promotion of Irish pigmeat on retail shelves.

- We aim to resume collaboration with Bord Bia on the revised Pigmeat Quality Assurance Scheme and the revision of pilot audits at the earliest appropriate opportunity.

- Active participation in the Pig Health Check Implementation Group, particularly in relation to the National Salmonella Control Programme and the Biosecurity Code of Practice.

- Continued work with the DAFM Welfare Division to ensure practical implementation of welfare policy that protects both animal wellbeing and farm sustainability.