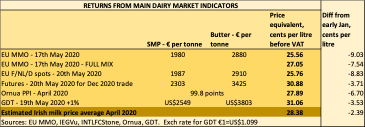

COVID19 has impacted dairy prices severely in early spring, with returns falling by over 9c/l based on EU MMO average market prices, and over 11c/l based on EU spot quotes between January and mid-April.

Recent trends have been more positive, with the introduction of a very limited APS scheme for dairy (see below) bringing a little more confidence, but more importantly, we have seen a very slow reopening of food services as more and more countries globally come out of lockdown creating demand to refill empty pipelines to respond to demand in a few months’ time.

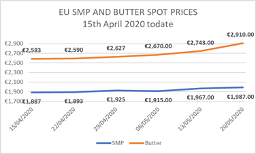

Spot quotes have increased week on week for over 4 weeks at this stage, and earlier this week the second GDT auction of May was up 1%, with a massive 6.7% increase in the SMP index.

EU average quotes are also firming, especially powders and butter, while cheddar cheese, which had held well todate, is easing somewhat.

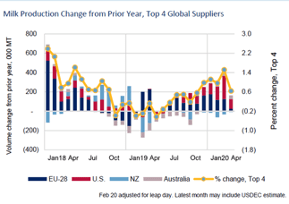

Milk supplies have been rising this spring in most regions bar New Zealand, and in Europe in most countries bar the UK and Denmark.Germany and France have seen much more moderate trends however, and analysts expect the second half of the year, influenced by poorer farmgate prices, to see lower levels of milk production growth.

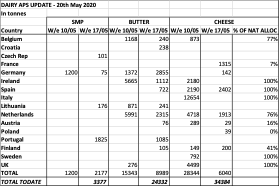

The COVID19 APS scheme opened for applications on 7th May, and Ireland had fully utilised its very modest 2180t cheese allocation within 3 days. By the second week of the scheme, around 38% of the overall 100,000t of cheese had been applied for, with Ireland joining many other countries who had fully utilised their allocation looking for reallocation of any unused quantities. Ireland has also contributed over 6,000t of butter, and no SMP. The table right shows the most recent data available on dairy APS utilisation all over Europe.

Milk prices had been cut by co-ops for March milk by up to 2c/l (Lakeland by 1.8c/l, Aurivo by 1.5c/l).

April milk price was further cut by another 1c/l, which could have been greater but for major IFA lobbying, in which the National Dairy Committee joined forces with the National Liquid Milk Committee, FMP and Co. Chairmen.

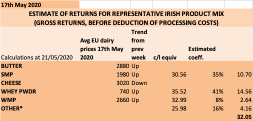

IFA estimates that April milk prices average at 28.38c/l + VAT (29.91c/l incl VAT) – however this average is a simple average of the FJ Milk League, and includes the 4 West Cork Co-ops which, even after a 1c/l total payout cut (half base, half contribution from Carbery Stability Fund) pay an April price of around 32.4c/l incl VAT.By comparison, Glanbia, Dairygold and Kerry pay an April milk price respectively of 28.42c/l, 28.69c/l and 29.5c/l – all VAT inclusive.

It is worth noting that Aurivo decided to hold their April milk price at the base March price of 30c/l incl VAT. (note, Aurivo also pays an unconditional early calving bonus of 1.48c/l for March milk, which obviously no longer applies to April milk).

Activity since last Council – including COVID-19 response

The Committee, in collaboration with our Liquid Milk colleagues and County Chairmen, has been actively lobbying board members to minimise the April milk price cut, by urging the review of every co-op’s profit and margin expectation, and by redirecting boards towards costs other than milk prices.While many co-ops had talked of milk price reductions in excess of 1c/l, none as we write have cut by more.

IFA is in weekly teleconference contact with DII and other stakeholders, including Teagasc, DAFM, ICOS and ICMSA to review developments in the processing sector.So far, collaborative contingency planning between co-ops and hard work by milk collecting and processing staff in every co-op has meant all milk has been collected and processed, and peak is now passed in many co-op areas. However, large quantities will continue to test capacity for several weeks, and there is greater nervousness around what has been happening in meat plants (fundamentally different in terms of staffing arrangements and scope for distancing in the workplace, but also in terms of worker cohorts, which in dairy plants are not predominantly immigrants accommodated and travelling to work in groups as is often the case in meat plants).

The Committee has been involved in analysing and reacting to the newly announced Farm to Fork and Biodiversity Strategies published this week by the EU Commission, participating in the webinar on this topic hosted by ICOS and addressed by Mairead McGuinness MEP.

We have also participated in Brexit discussions with Tanaiste Simon Coveney and Minister Helen McEntee, as the prospect for a no deal Brexit is raising its head again.

In anticipation of a likely emergency budget over the coming weeks, the Committee has also contributed to the drawing up of IFA’s pre-budget submission.

Upcoming issues

Within 2/3 weeks, co-ops will be determining their May milk prices. IFA will monitor market developments and communicate those, which we hope will continue on the current more positive trend, to officers and members. We will also articulate our lobbying arguments in advance of the early to mid-June dates by which boards will be making those decisions.

The renewal of the Nitrates derogation from 2021 is also coming up, and we have participated in a meeting with Teagasc to better understand the likely additional requirements, including a recalculation of the N load of a cow possibly from 85kgs to 89kgs (conservative figure), but also in terms of slurry storage requirements, spreading, and need to prove exports where farmers operate above 170kgs without derogation.As the Nitrates derogation is vital to the dairy sector, and bearing in mind the government formation talks involving the Green Party and their demands in those areas, the Committee has made a clear decision that will continue to work on this topic in conjunction with the Environment Committee.