Lockdown exit and government stimuli promote dairy demand and boost prices

The total disappearance of demand from the food services market (cafes, restaurants, institutional restaurants and school canteens) which followed the quasi global lockdown in March has hit dairy markets hard. Dairy commodity prices plummeted: butter fell 24% between early Jan and early May while SMP fell 27% roughly over the same period.

Since then, the gradual reopening of economies first in Asia, then in Europe, has allowed demand to slowly recover as supply pipeline are being replenished and consumer demand for food services returns tentatively in the new, socially distanced “normal”.

In most of Europe, we have seen phased reopening plans speeded up as the public health statistics appeared to justify it. Beyond Europe, especially in Asia, the reopening of food services is even further advanced, and trade is reported by some operators as improving more than heretofore, with demand from food services recovering to over 50% of normal while retail sales remain very strong.

While some operators warn that this is linked to the refilling of pipelines depleted by the lockdown, and may slow when those are full again, others report a very real improvement in trade.

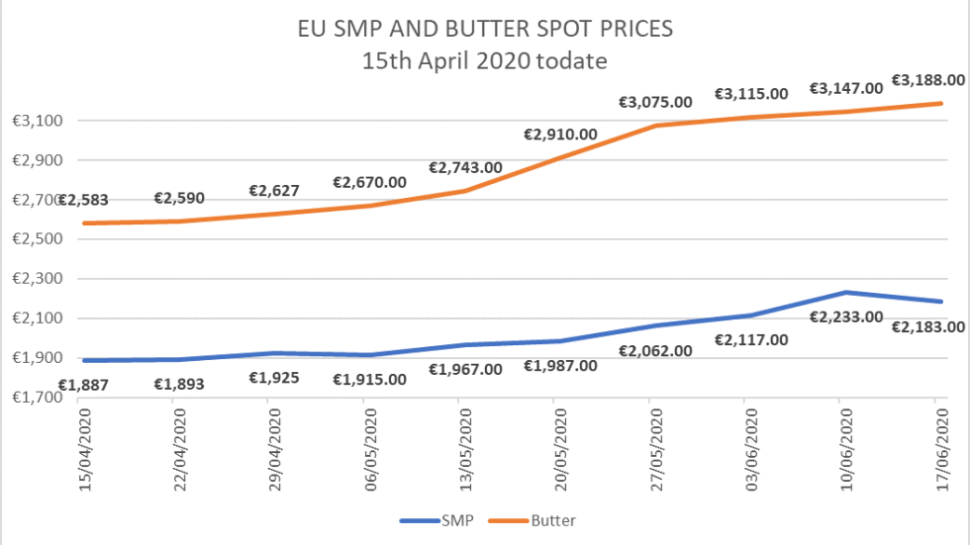

Based on data from INTL FCStone

The table below shows that EU exports have continued strong for the month of April and the Jan/April period, with the exception of SMP. EU exports of butter, butteroil (AMF), whey and pharmaceutical grade lactose have all increased substantially over the period, despite the pandemic.

This has allowed dairy product prices to recover substantially, though not yet to January 2020 equivalents. This has also helped stabilised May milk prices in Ireland, with Dairygold actually increasing its payout by 0.5c/l.

Source: INTL FCStone

Most market indicators have been showing improvements since mid-April, though they remain below January 2020 levels. However, most would appear to have reached levels that would underpin current milk prices, and possibly a small improvement. In the first table, the EU MMO average returns are given gross, before deduction of processing costs.

The first table below shows the gross (no processing cost deducted) returns from a representative Irish product mix, based on the most recent available prices reported by the EU Milk Market Observatory.

In the second table, showing the main national, EU and international dairy market indicator, returns have been calculated, to factor in a nominal 5c/l deducted from the returns to approximate the milk price equivalent of each indicator.

This is a convention rather than a precise processing cost: those are not independently published by any dairy company anywhere around the world. What is most valuable about monitoring indices is their evolution and changes up or down, as well as the pace of their change, so trends, rather than the absolute numbers.

The second table below shows that some returns have recovered up to half the fall that occurred between January and mid-April, and most appear to be still on an upward trend – which should augur well for at least the stability, or even improvement, of milk prices in the short to medium term at least.

Based on EU MMO data

Milk production rising to April, but…

With a lower than expected fall in milk prices and significant supports in the US, production has been rising more strongly into April in all regions except New Zealand.

Global April milk production is estimated to have increased 1.3% when compared to the same month last year.

For the January to April period, it is believed to have increased by 2.3%, which suggests a slowing trend.

Source: Bord Bia

European supplies have shown a similar dynamic, with April production up 0.8% and output over the January to April period up 1.6% leap-year adjusted according to the EU MMO, with significant differences between Member States (see graph below).

The April/May challenge to European production linked to moisture deficit has started to correct itself during June, with rain fall increasing in the most affected areas. However, it may be a case of too little too late for some regions, where it would have already impacted fodder production for the year.

Looking in more detail, the French April production reduction initiative appears to have borne fruit right till May, with output rising by only 0.6% in April, and falling into May. For the period from 1st April to the first week of June, INTL FCStone estimate French milk output was back 1.3%.

UK milk supplies, which the EU no longer accounts for as part of the EU 27, were also down 1.8% for the January to April period.

Source: EU MMO

APS provides mixed levels of support

As well as a slight moderation of some of the late spring/early summer output from some of the main dairy EU member states, we have seen some use of the EU Private Storage scheme which remains open for application till 30th June – and this will have had the effect of taking product temporarily off the market, especially butter.

The Cheese APS, which failed to recognise appropriately the importance of cheese to the Irish product mix, and only allocated Ireland a miserly 2180t filled within 3 days of the 7th May opening, is only 44% utilised todate – with only a few days to go to the closing date. While the Irish government has sought an opening of all allocations to allow for more use, this does not appear to have been accepted by the EU Commission.

Perhaps more helpful is the butter scheme, which has taken in almost 55,000t todate, with Ireland contributing 11,709t. Commentators suggested that maybe as much as a quarter of all butter made during the period went into APS – which would suggest optimism as to the price level to be expected when the product must come out next autumn.

The SMP scheme was only used to the tune of 13,178t, none of which from Ireland.

| Source: CLAL.it based on CME |

Massive US supports have also helped April to June dairy market improvements

In a recent global dairy market webinar by INTL FCStone, one of the US analysts stated categorically that the massive levels of supports given by the US Government in a bid to offset the disastrous economic impact of COVID 19 on US farmers’ prices and incomes had played a determining role in sustaining dairy prices globally.

Put more clearly, he suggested that the supports provided, which saw massive government food purchases, ensured that dairy commodity prices were supported, and massive price drops were could be corrected, avoiding a generalised collapse. The graphs for US butter and cheese prices show the impact of the purchasing supports very clearly.

Source: CLAL.it based on CME

Major direct supports were also paid to farmers – especially dairy farmers – but probably the most influential supports were connected to food purchases by government for distribution through food banks to needy Americans.

Also underpinning consumption, just like in most developed countries, significant supports were also given to employees and employers, including enhanced unemployment benefits to furloughed employees, and loans to employers, some of those becoming grants where jobs were preserved.

All of these sustained levels of internal demand which would have collapsed without them because of the economic impact of COVID 19.

A total immediate government relief programme of $19bn was spent in majority on direct farmer support, as follows:

- $16bn on direct support to farmers and ranchers based on actual losses

- $100m per month of purchases of dairy products for distribution (with other foods purchased under the same programme) through food boxes to US citizens in need;

- An additional $873.3m funding to purchase a variety of agricultural products for food banks;

- An additional $850m for food bank administration and USDA food purchases (of which a minimum $600m to be spend on food purchase)

- A variety of rural supports for loan deferment programmes, 100% grant projects;

- Etc.

Clouds on the horizon?

While dairy markets are performing better and returning improved prices, some commentators, not least Rabobank in their second Dairy Quarterly report for 2020, point out that the global economy will likely suffer a recession as governments in developed and emerging countries taper off the massive level of support they have given SME employers and employees.

The purchasing power of consumers, and their willingness/ability to spend will be challenged, which will likely impact consumption negatively.

For Ireland in particular, and Europe more generally, there is the small matter of the apparently increasing likelihood of a no-deal Brexit impacting from 1st January 2021.

However, the supports are unlikely to peter out too soon in the US, at least not this side of the next Presidential election in November.

In Europe, the COVID 19 support scheme of €750bn is in the process of being agreed by EU Member States, and should help kickstart recovery plans in all EU countries post COVID19 lockdown.

The market will continue to be difficult to predict. However, there is no sense in looking too far ahead in the context of an unprecedented pandemic.

For now, dairy markets underpin reasonably comfortably our current milk prices, and may even justify improvements.

Watch this space!