Grain Market Update 18th May

Domestic Market

Due to the continuation of the dry weather, feed demand has remained strong considering the time of year. If this dry spell continues, we will see an increase in the demand for supplementary feed as grass growth is adversely affected. The weather is beginning to have an effect on crops, with rainfall figures in areas of the midlands and east at record low levels for March and April. Parts of north Dublin have only received 45mm of rain in March and April and 4mm so far in May. This area would typically receive 160mm on average over these three months. At this stage rainfall amounts are actually lower than the bad drought year of 2018, however, on the plus side, crops were planted earlier this season and are better established than two years ago.

The figures on 2020 cereal plantings will soon be available from DAFM. They should show a cropping area for the main cereals of approximately 260,000 ha which would be similar to last season. In general, the reduction in Winter cropping area has been replaced by Spring crops. The combination of some poor Winter crops; the increased ratio of Spring crops and the possibility of an impending drought could see the production tonnage dropping below 2 million tonnes versus the 2.35 million figures in 2019.

While a considerable amount of barley remains in store, the stocks are lower than last year. IFA Grain Committee Chairman Mark Browne has called on feed mills to use Irish grains as feed merchants are now producing rations which contain little or no Irish grain and have replaced it with maize grain from non-EU sources.

The FOB Creil malting barley average price remains at €168/t. The plantings of malting barley have increased across the EU this season however some of this area increase has been mitigated due to the possibility of lower yields due to the dry conditions.

Irish Native / Import Dried Feed Prices 15/05/2020

| Spot €/t | Nov 2020 €/t | |

| Wheat | 198-202 | 190 |

| Feed Barley | 167-170 | 164 -168 |

| FOB Creil Malting Barley | 168 | |

| Oats | 160 | 160 |

| OSR | 360 | 360 |

| Maize (Import) | 180 | 173 |

| Soymeal (Import) | 348 | 340 |

International Markets

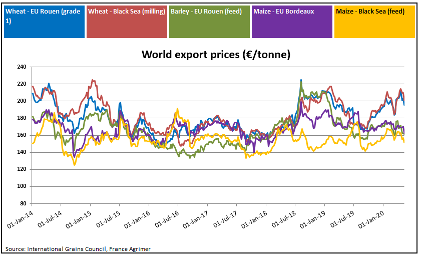

The wheat market reacted negatively to last week’s USDA’s report on the global wheat market outlook. They expect global wheat stocks at the end of the 2020/21 marketing year will rise to a record-large 310 million tonnes, up from 295 million at the end of 2019/20. However, these projections are based on best case scenarios and obviously weather could still play a part. The gap in prices between wheat and maize/barley is also significant and this could prove bearish for the crop. In relation to market positives, although parts of the Europe and the Black seas regions have received much needed moisture this may have been too little too late. In addition, exports of wheat from Europe have again been revised upwards which will leave less carryover stock going into the new season.

The USDA report proved somewhat benign for maize which is a slight positive. US maize prices are at historic lows due to the drop in ethanol demand and the prospects of record US plantings. However, prices have stabilised and market ending stocks are lower than predicted in the previous report with expectations of increased Chinese imports. Some market commentators predict US maize plantings to be lower than the governments figures and with ethanol demand picking up as economies reopen there is some optimism in the market.

In the soybean market, the USDA report was considered supportive with US production, US 2020/21 ending stocks and global ending stocks coming in below trade estimates. The increase in Chinese purchases is also seen as a positive for the market. Soymeal prices have continued to decline as world supply chains have returned to normal. As biofuel use begins to rise again rapeseed futures have remained strong. With EU rapeseed production predicted to be at historic lows of 17million tonnes, and with the EU’s main importer Ukraine also predicting lower production, spot prices should remain strong for the foreseeable future.