Domestic Market

Feed demand remains steady as the continued wet weather has ensured animals have remained indoors. Barley has picked up some demand due to the price differential with other feedstuffs, which will ensure lower stock levels than last year. Estimates would suggest that at this stage there are approximately 82,000 ha of Winter cereal crops planted.

This compares to the 154,000-ha planted for 2019 and 120,000 for 2018.We now have a situation where even if we get massive Spring plantings it will be difficult to reach the 2.35 million tonnes of production achieved last year. The industry expects that farmers may still plant significant acreage of spring wheat and beans if the weather allows in the next 10 days.

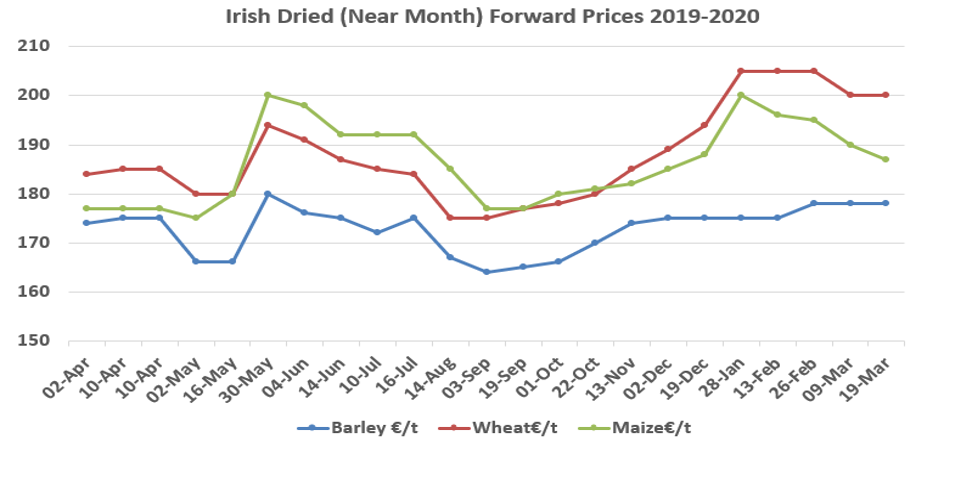

Irish Native / Import Dried Feed Prices 19/03/2020

| Spot €/t | May 2020 €/t | |

| Wheat | 196 | 200 |

| Barley | 170 – 175 | 178 |

| Oats | 160 | |

| OSR | 345 | |

| Maize (Import) | 187 | 187 |

| Soya (Import) | 372 | 355 |

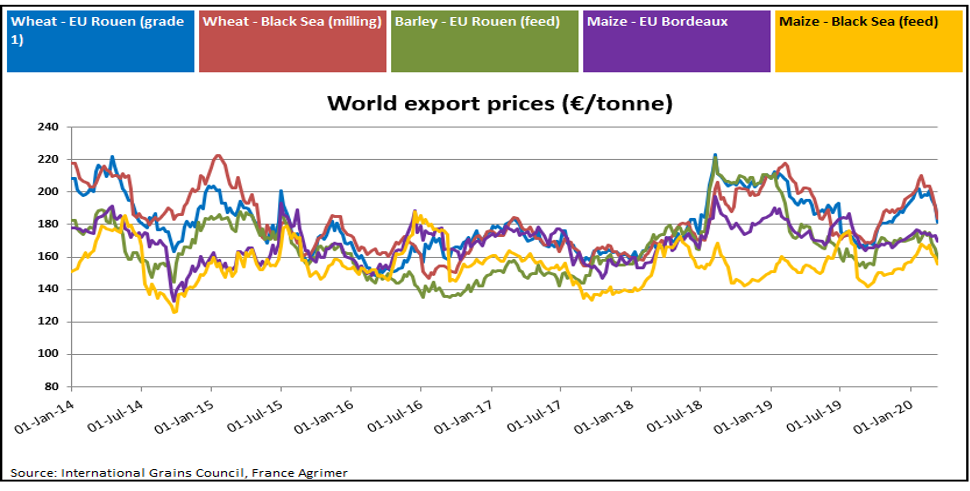

International Markets

Like all markets, the grain commodities have experienced extreme volatility in the recent week. The sudden drop in oil due to increased production from the Saudi’s has added further fuel to volatility already caused by the corona virus. Having dropped earlier in the week, wheat futures have made a remarkable comeback with the May Matif futures up by 10% in the past three days. Analyst say this is due to a combination of scarce stocks; increased demand for pasta; a weaker euro versus the dollar and an expectation of extra Chinese imports from the US as part of its Phase1 trade deal.

On the prospects for 2020 harvest, there are mixed reports from the Black sea region with some expecting Ukrainian production to be back by 10% on last year while Russian production could increase by a similar figure. Meanwhile in Europe, according to COCERAL, wheat production (excluding durum) is seen at 135.4 MMT down from last year’s 145.7 MMT. The EU’s 2020 barley production is now forecast at 61.5 MMT down from the 62.2 MMT last year. Due to the poor spring, French spring barley planting is only 40% complete which is behind the 5-year average, and compares to the 86% planted at this stage last year.

Corn (Maize) markets hit a four year low earlier in the week due to the collapse in ethanol demand, as it reacted to the collapse in oil prices. It has since strengthened from the oversold position, on renewed reports on an increase of Chinese imports of US corn. However, the prices could remain weak as the full impact of the corona virus pandemic on the world economy and subsequent consumption outlook remains uncertain.

In tandem with oil, all oilseeds have taken a hammering in recent weeks but have recovered somewhat in recent days. In contrast, soymeal prices have jumped considerably due to export issues from the world’s top exporter Argentina due to the corona virus outbreak and export tax issues. In addition, the expected collapse in ethanol production will leave less distillers grains available which will improve demand for soymeal. Rapeseed futures have fallen over 10% in the past month as all vegetable oils have come down in price. However, there should be support in the market at these levels due to the low estimates for European production again this season.