ARE OUR CO-OPS SHORTCHANGING US ON MILK PRICES?

- Co-ops are using our improved constituents and growing volumes to camouflage poor milk

prices

prices

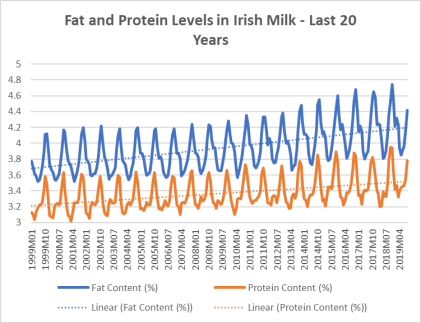

In the last 20 years, the mean annual protein content of the milk produced by Irish dairy farmers has gone from 3.2% to 3.5%, while butterfat levels have gone from 3.7% to 4.2%. Both constituents vary widely seasonally, with peak/trough differences of 0.6% for protein, and 1% for butterfat – the latter now unrestricted after the end of the quota regime.

Numerous co-ops have taken to quoting not only their standard price at 3.3% protein 3.6% butterfat, but also the price achievable in the relevant month at the co-op’s average constituents –especially so in autumn, when the constituents are at their seasonally highest levels.

Farmers have achieved those higher constituents through hard work, breeding, management and feeding, and have also grown volumes, also at a significant cost. They are frustrated to see their hard work being hijacked.

(Source of data in graph right: CSO)

- Co-ops have fallen behind the LTO

average, and have not reflected the European

average, and have not reflected the European

stable to firmer milk price trend in the last 6 months

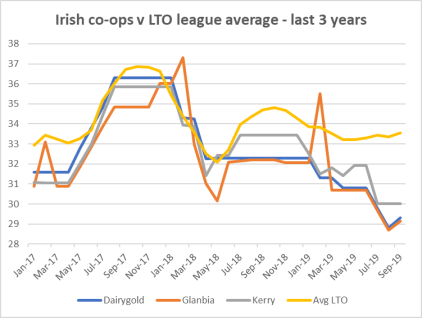

Three Irish co-ops are included in the LTO monthly European milk price league: Dairygold, Glanbia and Kerry. The LTO gathers milk statements from a small number of suppliers to each of the main milk purchasers in the main EU dairy countries. Prices are measured in €/100kgs, and standardised at 3.4% protein and 4.2% butterfat.

The graph to the right shows how the three Irish co-ops have fallen away and behind the LTO trend from May 18, and the gap between the Irish milk price and the LTO average has widened considerably in the last 18 months.

In effect, Irish co-ops have not followed the European milk price trend for at least 6 months, which is to stable or even firmer milk prices. Instead, Irish co-ops have continued cutting milk prices dramatically when European milk purchasers were holding, or even in some cases increasing, theirs.

Arguments made recently to suggest that lower Irish prices are due to our  commodity product mix versus larger consumer markets in Europe simply does not stand up in this context.

commodity product mix versus larger consumer markets in Europe simply does not stand up in this context.

(Source of data in graph above right: LTO Netherlands)

- Most co-ops have also fallen behind the Ornua PPI for most of the last 12 months

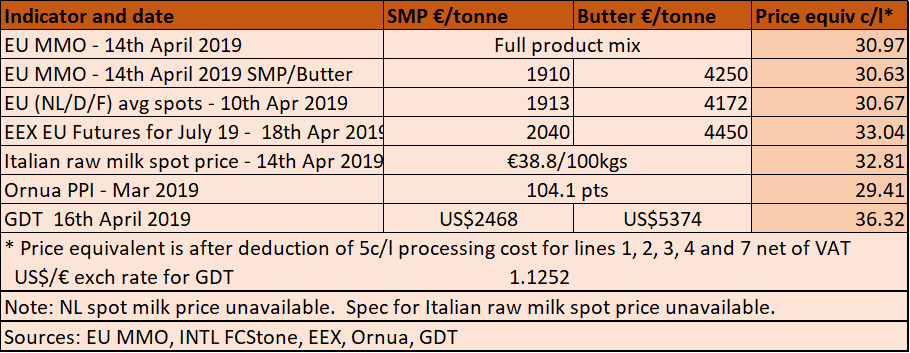

The Ornua PPI is probably the most directly relevant of all the dairy market indices IFA monitors, in that it reflects the exact product, market and price mixes traded on behalf of co-ops by Ornua for the month concerned.

Yet, from December 2018, all co-ops bar the four West Cork co-ops have fallen well behind for almost every single month.

The gap has widened to an October level of up to 2.5c/l – worth €1050 on the October supplies of a 500,000-litre supplier.

(Sources of data in graph right: Farmers’ Journal Milk Price League, Ornua)

WE NEED OUR CO-OPS TO DO BETTER ON MILK PRICES, AND THEY CAN!

- There are many market related reasons why co-ops can pay better milk prices

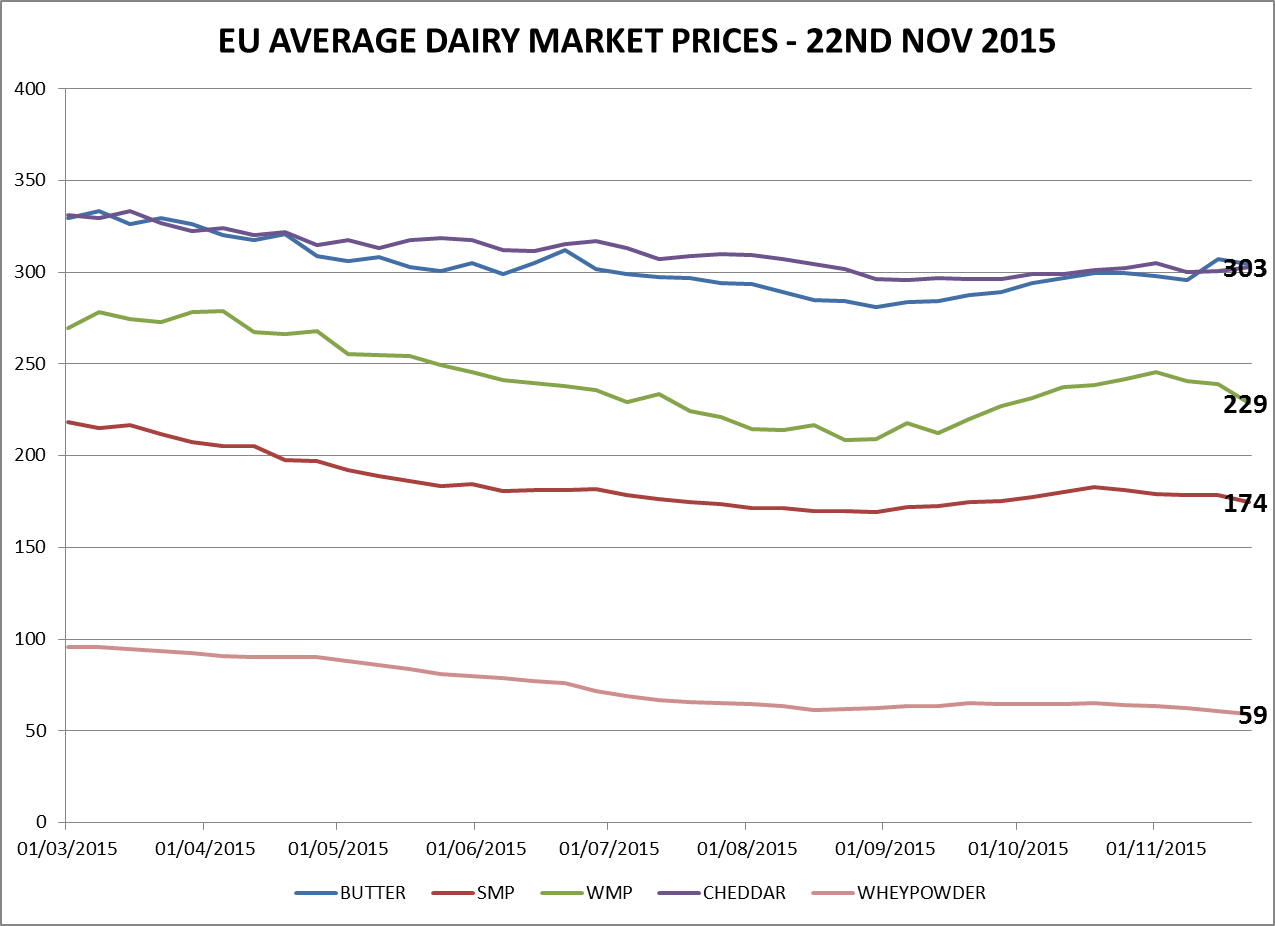

Subdued global dairy growth has been a feature for months.

It has led first to the rapid elimination of the intervention SMP stocks, and now to a real shortfall for 2019 and 2020 in privately held international stocks of powder.

SMP prices have risen by a whopping €340/t since early August!

While butter prices have come back, they had reached double their normal levels in 2017, and are now back to… their historically normal level! Also, they have firmed in recent weeks as the graph right shows.

Cheddar prices have lifted by €90/t since early August, WMP by €100/t and even whey powder prices (not featured in the graph right) have increased by €80/t over the period – an 11% lift.

(Source of data in graph right: EU Milk Market Observatory)

- Global markets have also improved

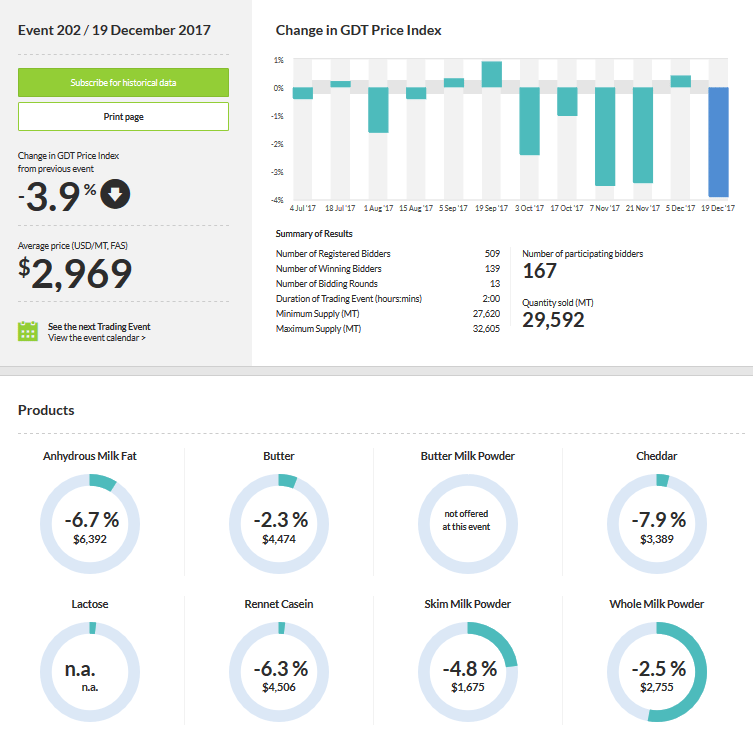

The last four GDT auctions have seen positive outcomes. We have seen a major increase in powders and protein prices: SMP is up 28% since June, and WMP up 12% over the same period.Since August, casein prices have increased 21%.Meanwhile, Cheddar and butter prices have been pretty stable, barely changing over the period.(Source: GDT) - Returns from the main indicators have firmed, and all are well above Irish milk pricesOver recent months, commodity prices

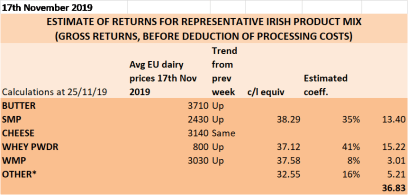

have either improved significantly (powders) or remained stable to firmer (cheese, and now, butter). European market indicators monitored by IFA have lifted throughout the period, and, futures excluded, return 1.4c/l to 5c/l more than Irish milk prices.The Irish product mix, based on the EU MMO returns since early August, has increased just over 2.5c/l (after deduction of a notional 5c/l processing cost).The Ornua PPI, which had been falling since May, has increased by 0.7c/l in the last 3 months.Spots and futures also suggest that those trends are set to last for the medium term at least.(Source of data in table right: EU MMO)

have either improved significantly (powders) or remained stable to firmer (cheese, and now, butter). European market indicators monitored by IFA have lifted throughout the period, and, futures excluded, return 1.4c/l to 5c/l more than Irish milk prices.The Irish product mix, based on the EU MMO returns since early August, has increased just over 2.5c/l (after deduction of a notional 5c/l processing cost).The Ornua PPI, which had been falling since May, has increased by 0.7c/l in the last 3 months.Spots and futures also suggest that those trends are set to last for the medium term at least.(Source of data in table right: EU MMO) - Farmers cannot afford poor prices next spring!

Merchant credit and other bills must get paid, and early heavy rain suggests a long costly winter and possibly spring ahead.Volumes are now stagnating versus last year, and constituents will dip at year end.Assuming no price changes from October, the March constituent levels will cost farmers around 3.8 cents per litre – that would be a cash-flow crippling €1600 shortfall on the March milk cheque for a 500,000-litre supplier.Our co-ops can, and must do better on milk prices this year end and next spring!

Merchant credit and other bills must get paid, and early heavy rain suggests a long costly winter and possibly spring ahead.Volumes are now stagnating versus last year, and constituents will dip at year end.Assuming no price changes from October, the March constituent levels will cost farmers around 3.8 cents per litre – that would be a cash-flow crippling €1600 shortfall on the March milk cheque for a 500,000-litre supplier.Our co-ops can, and must do better on milk prices this year end and next spring!